Neonatal intensive care, trauma care or burn care are among the services that could be hard to access in communities with high uninsured rates.

Much has been written lately about how individuals’ health could suffer if they lose insurance under the health proposals circulating in the U.S. House and Senate. But there is another consequence: creating millions more people without insurance could also impact the health of people who remain insured.

“We know that communities with higher rates of uninsurance have worse access to care for those with Medicare or private insurance,” said John Ayanian, director of the Institute for Healthcare Policy and Innovation at the University of Michigan. And if either of the GOP proposals now under consideration becomes law, he said, “it’s very likely we would go back to some of those same problems we had a decade ago with high rates of uninsurance.”

The Congressional Budget Office has estimated that either the bill passed by the House or the one under consideration in the Senate could result in more than 20 million more Americans without insurance over the next decade.

Ayanian was part of an expert panel from the nonpartisan National Academy of Medicine that examined the implications of being uninsured in a series of studies from 2001 to 2009. An entire report looked solely at the spillover impact of large numbers of uninsured people on those around them. “The Committee believes it both mistaken and dangerous to assume that the persistence of a sizable uninsured population in the United States harms only those who are uninsured,” said the report.

That is mostly because it is difficult for health providers to maintain services in areas with large numbers of patients who cannot pay for care. “Those communities are less attractive for physicians and other health care providers to locate,” said Ayanian. “That affects access to care for everyone,” he said, particularly for critical but high-cost services like trauma care, burn care, and neonatal intensive care.

The potential is not merely theoretical. Hospitals in sparsely populated areas, particularly in states that did not opt to expand the Medicaid program, have been cutting back services like maternity care or closing altogether in recent years. These are the same parts of the country that voted for President Donald Trump by large margins.

The impact is not just on availability of services. A 2007 study from researchers at the University of Pennsylvania in the journal Health Affairs found that in areas with many uninsured people, the quality of care was lower as well. Primary care doctors “reported that the higher the proportion of uninsured people in their community, the less likely they are to be able to refer their patients to high-quality specialists,” found the researchers. “Specialists also reported that the higher the community uninsurance rate, the less able they are to deliver high-quality care to their patients,” the study said.

That spillover effect even extends beyond access to health care itself, according to a new report from The Commonwealth Fund. Researchers from George Washington University found that if the House-passed health bill were to become law, nearly 1.5 million jobs could be lost over the next decade.

“We’re talking about a net funding loss to states of millions of dollars,” said Leighton Ku, the study’s lead author. “What this means is that states will have higher needs, less revenue to pay for services, and at the same time the federal government is putting less money into Medicaid,” he said. “So it all adds up to a great revenue crunch that’s similar to the Great Recession” of the past decade.

While most of the job loss would be in health care, other jobs would be impacted too, he said.

For example, health care workers who lose jobs will then purchase fewer goods and services, affecting the bottom line of local businesses. Health care facilities that were planning to expand might not, affecting the construction industry. And the impact could even cross state lines, said Ku. “We might see fewer people going to Disney World,” he said, because people who lose their jobs would lack money to take vacations.

Kaiser Health News, a nonprofit health newsroom whose stories appear in news outlets nationwide, is an editorially independent part of the Kaiser Family Foundation.

Senate Republicans introduced a revised version of their bill to repeal and replace the Affordable Care Act on Thursday, one that would allow insurers to once again deny coverage based on preexisting conditions, and to charge higher rates to sick people.

The bill would keep most of the Affordable Care Act’s tax increases but repeal one aimed specifically at medical device manufacturers. It would deeply cut the Medicaid program, making few changes to the bill’s first draft.

Even with these new changes, the general structure of the bill stays the same from its original draft, which was itself largely similar to the bill that passed the House in the spring.

Healthier and higher-income Americans would benefit from the changes in the new Republican plan, while low-income and sick Americans would be disadvantaged. It would create a two-track system for health coverage on the individual market. One would offer cheaper, deregulated health plans, which healthy people would likely flock to. The other would include comprehensive plans governed by Obamacare’s regulations, which would cost more and mostly be used by less healthy people and those with preexisting conditions — a system experts expect would function like a poorly funded high-risk pool.

Deductibles would almost certainly rise under the Republican plan, as would overall costs for low- and middle-income Americans. Individual market participants would have more options to purchase catastrophic coverage, an option likely to appeal to those with few health care costs.

Experts expect the changes will do little to change the Congressional Budget Office’s estimates that 22 million Americans would lose coverage under the proposal.

You can see a full explainer on the Senate bill here, which will be updated shortly with the latest information. This post focuses on the changes made in the July 13 revision.

Health insurers could bring back preexisting conditions, offer skimpy health plans

Perhaps the biggest policy change in this revision is an amendment to allow health insurers to deny coverage based on preexisting conditions and cover few benefits, so long as they offer a comprehensive plan that covers the Affordable Care Act’s mandated benefits.

These deregulated health plans would be allowed to charge sick people higher premiums or simply deny them coverage. They would not have to pay by the rules of the preexisting condition ban that the Affordable Care Act sets up (Phil Klein at the Washington Examiner has a summary of the rules they’d be exempted from here). Instead, they would operate much like health plans in the pre-Affordable Care Act market, offering cheap rates to consumers they believe would have low medical bills.

Health policy experts know exactly how this would play out: Healthy people would pick the skimpier plan, while the comprehensive plan would essentially become a high-risk pool for sicker Americans.

Individual market enrollees would likely game the system too. A couple expecting a baby, for example, would be expected to upgrade to the plan that covers maternity care for one year before returning to the cheaper plan they had before.

“Someone with chronic illness, they’re going to end up wanting to buy the more comprehensive coverage,” says Joe Antos, a health policy expert with the conservative American Enterprise Institute. “This means that people with those kinds of illnesses will end up paying more. Even if they receive a federal subsidy, they will likely see higher cost sharing.”

As Antos notes, individuals who want to buy the comprehensive plan would receive federal tax credits to do so. They could not use the tax credits for the deregulated plans.

But even after that financial help, these people would still face significant out-of-pocket costs, including high deductibles and premiums. The Congressional Budget Office estimates, for example, that a 64-year-old individual earning $11,500 and receiving tax credits would still need to pay $4,800 to purchase that plan.

The updated Senate bill also allows individuals to use tax credits to purchase catastrophic coverage

There is a quieter way the Senate bill lets people buy skimpier plans: by using their tax credits to purchase catastrophic plans.

This is a practice the Affordable Care Act barred, as the law’s drafters wanted to encourage enrollment in more generous options. But the Senate bill would allow the tax credits to be used for these high-deductible plans. These plans would only include three primary care visits before individuals hit their deductibles and have to pay their medical bills out of pocket. The plans could cover a wide array of health benefits, including maternity and mental health, but, again, coverage would only kick in after paying a large deductible.

The updated bill would let individuals use pre-tax dollars to pay for their premiums

An estimated 29 percent of American workers are enrolled in tax-advantaged health savings accounts (HSA), that allow them to use pre-tax dollars to cover things like copayments and coinsurance.

The Senate bill would allow HSA dollars to go toward premiums as well, meaning someone in the individual market could use pre-tax dollars to pay their monthly bill. This practice was not allowed under the Affordable Care Act.

Liberals have typically opposed this provision, which they argue would mainly benefit wealthy Americans who have the money to contribute to an HSA in the first place. This provision would have fewer benefits for low-income Americans, who rely on tax credits to finance the lion’s share of their premium.

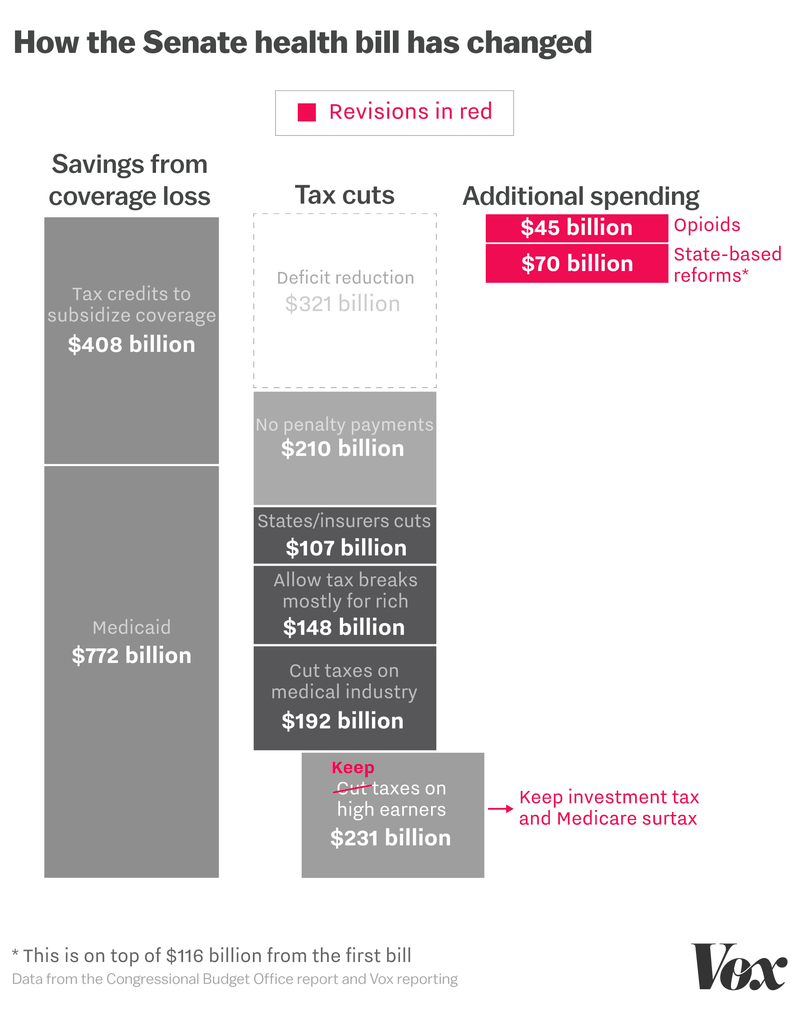

The Senate bill gets rid of most Obamacare tax cuts — but keeps two on high earners in place

The Senate’s revised health care bill still includes an estimated $657 billion in tax cuts by eliminating the health law’s taxes on the medical industry and its individual mandate penalty for not carrying coverage, among other changes.

It does continue two taxes aimed at wealthy Americans: a 0.9 percent investment tax and a 3.8 percent Medicare payroll surtax. Keeping these two taxes in place would net the government an estimated $231 billion in revenue over the next decade, and eliminate some of the benefits high-income Americans would have received under the first draft.

These new taxes, however, do not seem to be fully spent on enhancing the law’s benefits. The new bill includes a $45 billion program to combat opioid abuse as well as $70 billion to offset the costs of expensive patients (this is in addition to the $112 billion already appropriated for that purpose in the first version of the bill). The inclusion of these taxes does not appear to lead to any additional funding of the Medicaid program or offset any of the cuts to the tax credits in the individual market.

The Senate bill still makes very deep cuts to Medicaid

The Senate bill is notable in what it doesn’t change: namely, significant cuts to the Medicaid program. While moderate senators have protested these cuts (particularly those who represent Medicaid expansion states), these provisions of the Senate bill remain largely intact.

One of the main ways Obamacare increased insurance coverage was by expanding the Medicaid program to cover millions more low-income Americans. Prior to the health law, the entitlement was restricted to specific groups of low-income Americans (pregnant women, for example, and the blind and disabled).

Obamacare opened up the program to anyone below 138 percent of the poverty line (about $15,000 for an individual) in the 31 states (plus the District of Columbia) that opted to participate.

The Medicaid expansion gave states generous funding to cover this particular population. Typically, the federal government picks up about half the cost of the Medicaid program and states cover the rest.

For Medicaid expansion, however, the federal government currently pays 95 percent of the costs — an especially good deal for states meant to assuage their budget concerns during the original Obamacare debate.

The Senate bill would begin ratcheting down that Medicaid expansion funding in 2021. By 2024, states would get that same match rate they typically get to cover other populations. In 2021, for example, the match rate would fall to 90 percent, then decline in steps to 75 percent by 2023.

The Congressional Budget Office has projected in a separate analysis that this policy change would mean no additional states expand Medicaid — and that some current expansion states would drop out of the program, resulting in millions losing coverage.

“CBO anticipates some states that have already expanded their Medicaid programs would no longer offer that coverage,” the agency wrote in its analysis of the House bill, which makes a similar change.

The Senate bill would cut the rest of the Medicaid program too

There are significant changes to Medicaid in the Senate bill outside of the expansion too. This bill would convert Medicaid to a “per capita cap” system, where states would get a lump sum from the federal government for each enrollee. Or states would have the opportunity of a block grant — a sum of money untethered from the number of people involved.

This is very different from current Medicaid funding. Right now the federal government has an open-ended commitment to paying all of a Medicaid enrollee’s bills, regardless of how high they go.

The Senate bill would set different amounts for different groups of people. It envisions, for example, higher payments to cover Medicaid enrollees who are disabled (and tend to have higher costs) than for Medicaid enrollees who are kids (generally healthy with lower costs).

The rate at which these payments grow is also important. The Senate bill would have the funding growth tethered to the Medical Consumer Price Index plus 1 percentage point through 2025, and then switch to the urban Consumer Price Index. Analysis of this type of proposal suggests this change would amount to funding cuts for Medicaid, as the program’s spending typically goes up faster than these growth rates.

Sean Hannity’s name may rhyme with sanity, but Donald Trump’s favorite Fox has never been the poster boy for rationality. As the dominoes have started falling ever faster in the Trump–Russia scandal, Hannity has been bouncing all over the place in a storm of twisted logic, misplaced sarcasm, and desperate attempts at misdirection. But in the middle of this Hanni-cane, he actually dropped a line that’s … interesting.

“Why did the Obama administration let [the lawyer] into the country in 2016?” he asked.

Good question. And there’s a good answer.

Natalia Veselnitskaya did not mark up her visa application with “coming to America to give Donald Trump high-level information straight from the Kremlin.” Which, considering the stealth that Trump Junior displayed at the other end of the pipeline, is really rather surprising. Instead, Veselnitskaya’s official reason for coming to the United States really did have to do with the Magnitsky Act. Not lobbying against the act, but acting as an attorney in a lawsuit against a Russian company accused of money-laundering for the mob.

The specific case in question here is against Prevezon Holdings Ltd., a Cyprus-registered company.

How did Prevezon Holding supposedly move mob money into the United States? By snapping up expensive condos and other real estate. And who was it that Veselnitskaya had come to fight after she made her pitch to Donald Trump Junior?

U. S. District Attorney Preet Bharara.

In March, Donald Trump fired Bharara even though he had previously assured the US attorney that he would bestaying to complete current cases.

Mr. Bharara was a highly public prosecutor who relished the spotlight throughout more than seven years in office. He pursued several high-profile cases involving Wall Street, and he was in the midst of investigating fund-raising by Bill de Blasio, the mayor of New York, and preparing to try former top aides to the governor of New York, Andrew M. Cuomo, who are both Democrats. It was not immediately clear how his departure would affect those cases and others that were pending.

But Trump’s desire to get Bharara out of his office was unlikely to have anything to do with his willingness to go after Democratic targets as well as those on the right. Before his firing, Trump tried to make the same moves to secure the attorney’s loyalty that he had also made toward former FBI director James Comey.

“It appeared to be that he was trying to cultivate some kind of relationship [with me],” he told George Stephanopoulos on Sunday, citing several chummy phone calls that Trump tried to initiate with him. “It’s a very weird and peculiar thing for a one-on-one conversation without the attorney general, without warning, between the president and me or any United States attorney who has been asked to investigate various things and is in a position hypothetically to investigate business interests and associates of the president.”

But Donald Trump’s personal attorney has openly bragged that he was the one who told Trump to sack Bharara … for a very specific reason.

According to four sources that spoke to ProPublica, Marc Kasowitz, Trump’s personal lawyer and his primary counsel on matters related to the Russia investigation, had bragged that he was largely responsible for getting the U.S. attorney for New York’s Southern District fired. “This guy is going to get you,” Kasowitz recalled saying to Trump, according to one of the sources.

The connection between Bharara’s cases and Trump–Russia wasn’t immediately obvious. But Bharara hinted heavily that he had been ousted to close down a investigation of corruption related to Trump.

Until now, the case didn’t seem to be a peek into corruption inside the Trump regime. But with the spotlight now falling on Natalia Veselnitskaya, the actions of Prevezon Holdings Ltd are coming squarely to the center. Prevezon appears to be yet another holding company created expressly for the purpose of turning Russian mob money into American real estate in deals that allow oligarchs to clean their stolen funds and US real estate moguls to pocket fat profits. Deals exactly like those Trump is known to have used to escape bankruptcy.

When Donald Trump Jr. says that Veselnitskaya came to his office to discuss “adoption,” what he means is that she wanted to discuss the Magnitsky Act. And that discussion not only reflects on the US sanctions and blacklisting of Russian officials that resulted from the act, it directly plays into the Russian use of US real estate for money-laundering. Which was something Trump Jr. knew very, very well.

“Russians make up a pretty disproportionate cross-section of a lot of our assets,” Trump’s son, Donald Jr., told a real estate conference in 2008, according to an account posted on the website of eTurboNews, a trade publication. “We see a lot of money pouring in from Russia.”

So even the part of the conversation that Donald Trump Jr. has been passing off as “inane nonsense” was actually directly related to his business, and directly related to an investigation that Trump was anxious to see closed.

One more thing. No matter how many times Trump Jr. pretended to not know who Veselnitskaya was in his statements [Twitter page omitted] Emin Agalarov was more than just someone Trump Jr. had met during the Miss Universe pageant. He was a key contact for the Trump Organization, and their partner on potential deals in Moscow. Natalia Veselnitskaya was also clearly someone other than the nameless woman who showed up to give Trump Jr. a talk he didn’t want to hear. Both of them go right back to the core of Trump’s business—which was money laundering.

If all of this is making the world seem pretty small … it’s because it’s all connected. And the center of that connection is Donald Trump.

The Senate Better Care Reconciliation Act (BCRA), a proposal to repeal and replace the Affordable Care Act (ACA), includes a provision to create new association health plan options for small employers and self-employed individuals. These so-called “small business health plans” (SBHPs) would be considered part of the large group market, which has different rules than the small group market. In particular, the ACA requirement that premiums cannot vary based on health status does not apply in the large group market. Neither does the requirement for policies to cover ten categories of essential health benefits. If enacted, this provision would considerably disrupt the small group market because small employers could seek lower rates or less comprehensive coverage in an SBHP when their employees are healthy, but theoretically move back to regular small group market plans if an employee becomes ill or if the group wants more comprehensive benefits. This type of adverse selection could result in significant premium increases and instability in the small group market. The provision could disrupt the non-group market in a similar manner because it would permit self-employed individuals (in states that choose to regulate very small groups of one as small employers) to join SBHPs when they are healthy or want few benefits, but move back to regular non-group coverage if their health or circumstances change.

Background

Under the BCRA, new association health plan options would be available to small employers and to the self-employed in certain states. The bill amends the federal Employee Retirement Income Security Act of 1974 (ERISA) to establish the following rules, standards, and definitions for small business health plans:

Large group market rules apply. A SBHP is defined as a fully insured group health plan, sponsored by a certified entity, and offered by a health insurer in the large group market. Several key requirements for small group market insurers do not apply in the large group market. Insurers in the small group market cannot consider the health or claims of a small group’s employees, and must cover the 10 categories of essential health benefits (though states could waive that requirement under the BCRA). These rules do not apply in the large group market. The BCRA sets no standards for SBHPs in terms of what benefits must be covered or how premiums would be set for small firms that want to participate. For example, the insurer covering the SBHP could medically screen small firms applying, and charge relatively low rates for healthy groups but very high rates for groups with sick employees. In addition, the insurer could consider a group’s health and claims at renewal and give them considerably higher rate increases than other groups. The same practices could apply to self-employed individuals. Small businesses could join and enroll in SBHPs, as could self-employed individuals with no other participating employees (i.e., groups of one) in states that choose to regulate such arrangements as small group health insurance.

Federally regulated. The sponsor of a SBHP must be certified by the Secretary of Labor. Federal certification is deemed approved after 90 days unless the Secretary denies the application for cause. To do business in a state, a certified SBHP must provide written notice of its certification to the insurance regulator in every state in which it will operate. The federal government also has enforcement authority over the business practices of SBHPs. The bill includes broad preemption language stating that federal standards “shall supersede any and all State laws insofar as they may now or hereafter preclude a health insurance issuer from offering health insurance coverage in connection with a [certified] small business health plan.” This appears to prohibit a state from requiring that a SBHP be regulated as small group coverage and may preempt other state insurance rules, as well. The Secretary is required to coordinate with the State in which a particular SBHP is domiciled regarding the exercise of federal authority to certify a SBHP and enforce federal standards. The Secretary is also required to ensure that only one domicile state will be recognized with respect to any particular SBHP. The bill does not provide that the rules of the domicile state will supersede the laws of other states.

Nondiscrimination standards. The entity that sponsors a SBHP must be organized for a purpose other than providing health benefits, although it appears that providing health benefits could be the primary purpose of the organization. For example, a sponsoring entity could be a bona fide trade association, organized primarily for professional or industry-related purposes. Or it could adopt broadly inclusive membership standards to permit virtually any small group or individual to join. In addition, the sponsor of the SBHP is prohibited from conditioning membership on the size of its member groups. The bill does not prohibit a sponsoring entity from conditioning membership on the health status of small businesses; a nondiscrimination provision in the bill states that a requirement not to discriminate against employers and eligible employees is satisfied if the SBHP makes information about all coverage options readily available to any eligible small employer.

Under the BCRA, the SBHP provisions become effective 1 year after the date of enactment and the Secretary of Labor is required to issue implementing regulations no later than 6 months after the date of enactment.

Effects on Small Employers, Self-Employed Persons, and Traditional Markets

The establishment of small business health plans could affect the way health insurance operates for small employers, and could affect the entire small group health insurance market, in several ways:

Premium instability for small businesses and self-employed individuals – Because SBHPs would be able to set premiums for small firm and self-employed members based on health and risk status, it could be possible for SBHP members to obtain lower premiums for coverage as long as their workers and their family members are healthy. However, in the event a covered individual becomes seriously ill or injured, nothing under federal law would prevent the SBHP insurer from raising the premium for that small employer or self-employed individual, even to unaffordable levels. The affected small employer or self-employed person might then try to seek coverage in the traditional small group market or non-group market, where health status rating is prohibited, though as discussed below, premiums there could also become unaffordable.

Increased premiums in traditional small group and non-group markets – Selection of coverage options, based on which market rules are most advantageous at the time, is sometimes called adverse selection. The asymmetry of rules applied to SBHPs and the traditional small group market would tend to segment small employers based on risk, steering more expensive groups to the traditional market and driving up community rated premiums. This could lead to premiums in the traditional small group market becoming much higher for employers who need to seek coverage there. Eventually, the impact of selection could force insurers to stop offering traditional small group coverage because they could not predict the risk of potential enrollees. The SBHPs would also be open to self-employed individuals in states that permit very small groups of one to buy small group coverage, as 14 states did prior to the ACA. In 2014, one in five marketplace consumers was a small business owner or self-employed. As a result, adverse selection from SBHPs could also affect premiums in the individual market.

Lack of clear regulatory authority – The BCRA requires that SBHPs must be fully insured group health plans, suggesting that states would continue to have regulatory authority over the insurance product itself, for example, to apply and enforce state standards related to risk based capital and solvency. However, preemption language in the bill is broad, and does not specify which state laws could still be enforced, including for example, laws relating to qualifications of SBHP sponsoring entities, or the covered benefits or rating practices under such plans. At a minimum, it seems legal challenges could arise if states would try to regulate SBHPs more closely. In the past, in response to federal proposals to create new small group insurance arrangements that would not be subject to all state small group market regulation, the National Association of Insurance Commissioners, the American Academy of Actuaries, and others have raised concerns that market fragmentation and harm to small businesses and consumers could result.

Discussion

The Senate SBHP proposal sets up competing and unequal regulatory regimes for small group health insurance that could undermine the traditional market. It also would potentially increase non-group premiums because healthy self-employed people could leave that market while people with health problems would not qualify for SBHP rates. In addition, small groups and the self-employed could choose less comprehensive policies while they are healthy, but move to more comprehensive plans if their health changed (if they remain available). Such adverse selection could drive up the cost of coverage in these markets, making health insurance less affordable for sick individuals and small groups who would have to rely on them, and potentially not available at all.

As the Senate considers the Better Care Reconciliation Act (BCRA), a proposal to repeal and replace the Affordable Care Act (ACA), amendments have been discussed to further change private health insurance market rules that apply under current law. Under the BCRA, current law health insurance market rules would still apply: Insurers in the non-group health insurance market are prohibited from turning applicants down or charging higher premiums based on health status and from excluding coverage for pre-existing conditions. In addition, all policies must provide major medical coverage for 10 categories of essential health benefits and must limit the annual out-of-pocket cost sharing (deductibles, co-pays and coinsurance) that people must pay for covered services in network (although states can alter those requirements through waivers).

However, an amendment to the BCRA, suggested by Senator Ted Cruz (R-TX), reportedly would allow insurers in the non-group market to also sell some policies that would not be required to follow all of the ACA market rules. For example, such policies might not have to follow ACA essential health benefit and cost sharing standards. In addition, some reports suggest that insurers would not have to sell these policies to people with health conditions or risks and could vary premiums for them based on the health of applicants.

This brief examines the likely impact of such a change on the stability of coverage offered through non-group markets and on the number of individuals who might be affected.

Impact on Consumers Ineligible for Premium Subsidies

If the BCRA were amended to permit insurers to sell ACA-compliant plans alongside plans that did not follow ACA-benefit standards and/or rating and access rules, the likely result would be that the cost of ACA-compliant plans would skyrocket. The ACA-compliant plans would effectively become a high-risk pool, attracting enrollees when they need costly health benefits – such as maternity care, or drugs to treat cancer or HIV, or therapies to treat mental health and substance abuse disorders – and those with pre-existing conditions who are turned down by non-compliant plans or charged high premiums based on their health. By contrast, non-compliant plans would attract healthier consumers, at least as long as they didn’t need coverage for such benefits. Premiums from the healthier enrollees would not be pooled to help keep the price of compliant plans affordable. As a result, premiums for compliant plans would increase significantly, while premiums for non-compliant plans would be substantially lower (though they would also cover fewer benefits).

The Senate BCRA would continue ACA-like premium tax credits to subsidize the cost of coverage for low-and middle-income individuals. Like the ACA, premium tax credits under the BCRA would be tied to the cost of a benchmark marketplace plan, though the benchmark would have higher patient cost-sharing than under the ACA. Eligibility for premium tax credits would be capped at income of 350% of the federal poverty level (FPL), compared to 400% FPL under current law. Individuals eligible for tax credits would be required to pay a set percentage of their annual income toward a benchmark plan; the premium tax credit amount for each individual would be the difference between the actual cost of the benchmark plan and a person’s required contribution. Under this formula, as under current law, subsidy-eligible people would generally be shielded from annual premium cost increases, which would instead be absorbed by federal premium tax credits.

While people with pre-existing conditions eligible for premium tax credits would be cushioned from premium increases in compliant plans under the Cruz amendment, those ineligible for credits would not be protected.

According to the National Health Interview Survey, approximately 40% of non-group market participants in 2015, or 6.1 million people, had income above 350% FPL. Most of these individuals purchased non-group coverage outside of the marketplace. Under the BCRA, these individuals would not be eligible for premium tax credits.

We further estimate that, among the 6.1 million non-group market participants with incomes of at least 350% FPL, 24% (or about 1.5 million) would have pre-existing conditions that would have been considered automatically deniable by insurers prior to the ACA. These conditions include cancer, diabetes, HIV/AIDS, hepatitis, substance use disorders (including opioid addiction), serious mental illnesses, and pregnancy. (Figure 1)

For these 1.5 million individuals, non-compliant plans would likely either deny coverage outright or charge very high premiums tied to their health. Even if they could obtain coverage in non-compliant plans, it might not cover key benefits, such as maternity care, mental health care, substance use treatment, or prescription drugs, and would not solve the affordability problem.

Among the three-quarters of other market participants with income over 350% FPL, millions would have other types of pre-existing conditions that were not considered automatically declinable prior to ACA, such as high-blood pressure, high cholesterol, asthma, and depression. Many in this group also could see a substantial increase in out-of-pocket spending for medical care that would offset any premium savings associated with less comprehensive policies.

Methods

To calculate nationwide prevalence rates of declinable health conditions, we reviewed the survey responses of nonelderly adults for all question items shown in Methods Table 1 using the CDC’s 2015 National Health Interview Survey (NHIS). Approximately 27% of 18-64 year olds, or 52 million nonelderly adults, reported having at least one of these declinable conditions in response to the 2015 survey. For more details on methods and a list of declinable conditions included in this analysis, see our earlier brief: Pre-existing Conditions and Medical Underwriting in the Individual Insurance Market Prior to the ACA.

The programming code, written using the statistical computing package R, is available upon request for people interested in replicating this approach for their own analysis.

Donald Trump, Aras Agalarov and Rob Goldstone. (Photos: Sean Gallup/Getty Images; Sergei SavostyanovTASS via Getty Images; Adriel Reboh/Patrick McMullan via Getty Images

While in Moscow for the Miss Universe pageant in November 2013, Donald Trump entered into a formal business deal with Aras Agalarov, a Russian oligarch close to Vladimir Putin, to construct a Trump Tower in the Russian capital. He later assigned his son, Donald Trump Jr., to oversee the project, according to Rob Goldstone, the British publicist who arranged the controversial 2016 meeting between the younger Trump and a Kremlin-linked lawyer.

Trump has dismissed the idea he had any business deals in Russia, saying at one point last October, “I have nothing to do with Russia.”

But Goldstone’s account, provided in an extensive interview in March in New York, offers new details of the proposed Trump project that appears to have been further along than most previous reports have suggested, and even included a trip by Ivanka Trump to Moscow to identify potential sites.

According to the publicist, the project — structured as a licensing deal in which Agalarov would build the tower with Trump’s name on it — was only abandoned after the Russian economy floundered. The economic downturn resulted in part from sanctions imposed by the U.S. and the European Union following Russia’s intervention in Ukraine.

Goldstone’s version of events implies a possible explanation for Trump’s interest in lifting sanctions on Russia — a policy move his administration quietly pursued in its first few weeks until it ran into strong opposition from members of Congress and officials within the State Department.

Goldstone placed Donald Trump Jr. at the center of the Trump Tower deal, saying that his father assigned his eldest son the job of moving the project to fruition after the signing of a “letter of intent” between the Trump Organization and Agalarov’s company, the Crocus Group. It is not clear if the future president personally signed the “letter of intent,” but Michael Cohen, a longtime lawyer for Trump, told Yahoo News Tuesday that it would have been standard practice for Trump, as president of the Trump Organization, to do so.

Donald Trump Jr. at the Republican National Convention in Cleveland, July 18, 2016. (Photo: Jonathan Ernst/Reuters

Goldstone also said that Ivanka Trump flew to Moscow in 2014 and met with Emin Agalarov, the oligarch’s son, a pop singer and a vice president of the Crocus Group, to identify sites for the project.

Trump “put Donald Jr. in charge and then Ivanka went to Moscow to look around for what the location would be,” Goldstone said. But the plans for a Trump Tower fell apart because “the economy tanked in Russia’’ after the imposition of Western sanctions, he said.

Goldstone, a British-born publicist who once did worked for Michael Jackson, represents Emin Agalarov in his music career and was present in Moscow during the Miss Universe pageant when the Trump Tower project was discussed by Trump and Aras Agalarov. His role has gotten new attention this week after the New York Times disclosed that Goldstone emailed Donald Trump Jr. in June 2016 urging him to meet with a Russian lawyer to receive damaging information from the Russian government about Hillary Clinton.

Trump Jr. released his email exchange with Goldstone on Tuesday, confirming the key role of the publicist and, more significantly, the Agalarovs, in offering negative information about Clinton on behalf of the Kremlin. “Emin just called and asked me to contact you with something very interesting,” Goldstone wrote Trump Jr. on June 3, 2016.

A chief prosecutor in Russia “offered to provide the Trump campaign some official documents and information that would incriminate Hillary and would be very useful to your father. This is very high-level and sensitive information but is part of Russia and its government’s support of Mr. Trump — helped along by Aras and Emin.”

Alan Garten, the chief lawyer for the Trump Organization, did not respond to requests for comment. In a telephone interview, Cohen, who is Trump’s personal lawyer, did not dispute any specific details of Goldstone’s account but offered to check them. He did not later respond. But Cohen adamantly rejected the idea there was anything improper about meeting with the Russian lawyer, Natalia Veselnitskaya, given that Trump Jr. was told she might have information helpful to Trump’s campaign. “The purpose of the election is to win,” said Cohen, adding, “Why is this any different?” than the unverified “dossier” on Trump’s ties to Russia prepared by a former British spy working for a Washington research firm hired by his political opponents.

Trump Jr., accompanied by then campaign manager Paul Manafort and senior adviser Jared Kushner, met with the Russian lawyer at Goldstone’s request to review the information she purported to have. “He met with her face-to-face to determine” the validity of the advertised documents and “no information was provided.”

Goldstone had played a key role in helping to broker the initial decision by the Miss Universe pageant — then owned by the Trump Organization and NBC — to hold its 2013 contest in Moscow.

View photos

According to Goldstone, he pitched the idea to Paula Schugart, then chief executive of Miss Universe, as a way to promote the music career of Emin Agalarov. Schugart was initially hesitant because of concerns about red tape in Moscow. “What if you had a partner who owns the biggest venue in Moscow?” Emin Agalarov responded, according to Goldstone’s account. “Between myself and my father, we can cut through the red tape. You have a new partner.”

The plans to bring Miss Universe to Moscow was announced by Trump in Las Vegas in June 2013 during the Miss USA contest. Trump at the time quickly expressed hope that it would lead to a meeting with Putin. “Do you think Putin will be going to the Miss Universe pageant in November in Moscow — if so, will he become my new best friend?” Trump had tweeted at the time.

A meeting with Putin never came off during Trump’s Moscow trip; the Kremlin expressed regret that the Russian president wouldn’t be able to fit it into his schedule on the day in question because he had a meeting with the King of Holland. But the trip gave Trump an opportunity to discuss the plans for the Trump Tower in Moscow with Agalarov, a billionaire who has been called “the Trump of Russia” and “Putin’s builder” because of massive construction projects he has done on behalf of the Kremlin. Just 10 days before the Miss Universe pageant, Putin had given Agalarov a prestigious award at a ceremony at the Kremlin: Order of Honor of the Russian Federation.

In an interview with Forbes this March, Emin Agalarov confirmed the plans for Trump Tower in Moscow. “We thought that building a Trump Tower next to an Agalarov tower — having the two big names — could be a really cool project to execute,” Emin Agalarov told the magazine. Agalarov blamed the abandonment of the project on Trump’s decision to run for president, rather than the imposition of sanctions. “He ran for president, so we dropped the idea,” Agalarov said. “But if he hadn’t run, we would probably be in the construction phase today.”

But Emin Agalarov said he and the now president have continued to stay in touch, saying that Trump sent a handwritten note to the Agalaovs in November after they congratulated him on his victory. “Now that he ran and was elected, he does not forget his friends.”

New York was one of only two states to take advantage of the Essential Plan, also known as the Basic Health Plan, a program funded with the Affordable Care Act’s tax credits and cost-sharing subsidies. | Getty

ALBANY — The Senate’s version of the American Health Care Act would cost New York’s Medicaid program billions of dollars over the next decade, putting Albany in the position of having to choose between raising taxes or cutting services and programs for hundreds of thousands.

The bill, which is certain to change before coming to a vote, would also upend New York’s individual health insurance market, likely saddling many with higher deductibles and more expensive premiums.

“The Senate bill presented today, which was crafted behind closed doors by 13 men, would fundamentally harm Americans young and old, do severe damage to a fragile economy, and bankrupt state governments across the country,” Sen. Kirsten Gillibrand said in a statement. “The cuts to Medicaid in particular are galling. … To end the Medicaid expansion created under the Affordable Care Act is a cruel joke.”

The state’s Essential Plan, which enrolls nearly 700,000 New Yorkers in low-cost health insurance plans, likely would not survive in its current form because it relies on federal funding that would disappear. The program provides health insurance for $20 per month to those with incomes between 150 percent and 200 percent of the federal poverty level. Those with incomes below 150 percent of the federal poverty level, who do not qualify for Medicaid, receive health insurance with no premium.

New York was one of only two states to take advantage of the Essential Plan, also known as the Basic Health Plan, a program funded with the Affordable Care Act’s tax credits and cost-sharing subsidies. The cost sharing subsidies disappear in 2020 under the Senate’s version of the bill.

That would, on its own, be enough to severely handicap the Essential Plan but Republicans also propose prohibiting “lawfully present” immigrants from receiving tax credits. In New York, there are a couple of hundred thousand lawfully residing immigrants taking advantage of the Essential Plan. Without their tax credits, the state would have no method for funding their health insurance unless Albany decided to subsidize the insurance without federal help, a multi-billion dollar proposition.

A 2001 state Court of Appeals ruling requires that those residents, known as People Residing Under the Color of Law, receive Medicaid, which the state would once again have to pay for without any help from the federal government. That alone would cost the state $1.19 billion, according to an estimate from the state Department of Health.

On top of that, the Senate bill includes an amendment sponsored by Reps. John Faso and Chris Collins that would effectively prohibit the state from using county taxes to pay for the Medicaid program. That is expected to shift roughly $2.3 billion from county budgets to the state budget, and though it may ease the property tax burden in upstate New York, it will do nothing to ease the budget woes facing Albany in 2019.

The more severe Medicaid cuts would hit between 2020 and 2024, according to the Senate bill, which phases out the enhanced federal match states such as New York received from the federal government because of Obamacare.

In its place, there would be a per-capita cap assigned to each state. The per-capita cap would be based on what a state spent between 2014 and 2017, but high-cost states such as New York would see their per capita reduced by the secretary of Health and Human Services by as much as 2 percent.

Shoppers on the individual insurance market would see the value of their subsidies decrease. The Affordable Care Act pegged subsidies to a silver plan, which has an actuarial value of 70 percent, meaning insurers pay for 70 percent of the costs. The Senate version pegs subsidies to plans with an actuarial value of 58 percent. That will almost certainly mean New Yorkers who rely on subsidies will need to purchase skimpier plans with higher deductibles. Those who wish to buy the equivalent of silver plan will spend more out of their pocket on premiums.

The cutoff for income-based subsidies under the Senate plan is reduced to 350 percent ($42,210 for an individual) of the federal poverty level from 400 percent. Subsidies tied to the federal poverty level always hurt high-cost states such as New York where incomes tend to be higher than average, as does the cost of living. Basically, $43,000 goes a lot further in most other parts of the country so subsidies for health insurance aren’t as needed.

The Senate’s version is also worse for New York hospitals compared to the House version, according to the Greater New York Hospital Association, which pointed out that the House bill repeals the cuts to the Disproportionate Share Hospital program for Medicaid expansion states in 2020. The Senate does not, costing hospitals billions of dollars.

“It’s every bit as bad as the House bill. In some ways, it’s even worse,” Senate Minority Leader Chuck Schumer said Thursday on the floor of the Senate. “The president said the Senate bill needed heart. The way this bill cuts health care is heartless. The president said the House bill was mean. The Senate bill may be meaner.”

The state Department of Health would not provide an estimate of how many people with incomes between 350 and 400 percent of the federal poverty level buy plans on the exchange, although the state does collect income information.

The agency also declined to predict the total cost of the Senate’s bill on New York, or its effects on the Essential Plan, providers or insurers.

From left, Senate Majority Leader Mitch McConnell and Sens. Pat Roberts (R-Kan.) and Steve Daines (R-Mont.) chat before a Republican meeting to discuss the health care bill on June 27. (Nicholas Kamm/AFP/Getty Images)

Montana was among the last states to expand Medicaid, and its Obamacare marketplace has fared reasonably well. It has 50,000 customers, decent competition and no “bare counties,” where no insurers want to sell plans.

The Republicans who make up two-thirds of Montana’s congressional delegation have said they want to repeal the current health care law because it’s causing health insurance markets to “collapse.”

But insurance executives at the companies that sell policies in Montana’s marketplace say that’s not true in the state, and they are concerned that GOP plans to repeal and replace the Affordable Care Act would destabilize a market that is working. Jerry Dworak, the CEO of Montana Health Co-Op, said, “I don’t think that their plan is going to improve health care in the state of Montana. I think just the opposite is going to happen. And I really do think a lot of people are going to get hurt.”

The co-op is one of the three insurance companies that have been selling Montanans coverage at healthcare.gov since it started in 2013. Dworak said it has no plans to leave.

The executives say collapse is a real possibility, though, if some of the GOP’s wish list comes true. First, deep cuts to Medicaid would have ripple effects to everybody with insurance. Todd Lovshin, a vice president at PacificSource Health Plans, said Medicaid expansion means Montana hospitals are now getting paid for taking care of more than 70,000 Montanans who got Medicaid after the state expanded it under the Affordable Care Act.

“All of our hospitals have to take any patient that comes in and serve them. That has to be paid somewhere,” he said. “And if we’re not paying that through Medicaid expansion, those costs have to be borne by someone, and so that will increase the overall cost of medical expenses.”

Hospitals have a legal obligation to examine and stabilize any patient who walks in their door, regardless of whether they have insurance. When hospitals see their unpaid bills stack up, Lovshin said, prices go up for everybody else and insurers have to charge patients who have insurance more to stay afloat.

John Doran, a vice president with Blue Cross and Blue Shield of Montana, the state’s biggest insurer, agreed with that analysis.

Doran also said that problems would likely get worse if the individual mandate goes away. That’s the requirement to have health insurance that Republican health care bills do away with.

“If there’s no mandate, and there’s no incentive for them to buy a health insurance plan, then maybe they won’t,” he said. “The people who need health care the most, and typically have the highest health care costs, are the only ones who are in the marketplace, and that results in higher health care costs, and consequently higher premiums.”

Montanans have been seeing insurance premiums go up, sometimes by more than 50 percent a year. Most people who buy on the exchange get subsidies to help defray the cost, and the co-op’s Dworak said he thinks prices are now starting to stabilize. If the health law isn’t changed, he projects his company’s premiums would go up only 5 percent in 2018.

This story is part of a partnership that includes Montana Public Radio, NPR and Kaiser Health News.

Kaiser Health News, a nonprofit health newsroom whose stories appear in news outlets nationwide, is an editorially independent part of the Kaiser Family Foundation.

The Commonwealth Fund predicted an additional 753,000 jobs in 2018, but employment numbers would drop sharply after that. It said every state except Hawaii would have fewer jobs and a weaker economy. States that expanded Medicaid would feel the most pain.

The report came out on the same day that the Bureau of Labor Statisticssaid 37,000 healthcare jobs were added in June, up from 20,600 added in May .

Dive Insight:

The Commonwealth Fund said that job losses and lower economic growth would begin in 2020 and deepen in the following years as more people lose health insurance coverage, if the Senate bill were to become law.

The House’s American Health Care Act (AHCA) would cut a similar number of insured Americans, but the BCRA would harm the economy more, according to the report. The Commonwealth Fund estimates the AHCA would result in nearly 1 million lost jobs.

New York, California and Pennsylvania would lose more than 100,000 jobs each. “Twenty-two million Americans will become uninsured under the Better Care Reconciliation Act, and now this research makes it clear that people will also be at risk of losing their jobs and that states’ economies will suffer,” said Sara Collins, vice president for healthcare coverage and access at The Commonwealth Fund.

One reason for the economic problems resulting from the BCRA is the bill’s Medicaid cuts, which would deepen further after 2026. Also, the BCRA’s tax provisions would result in much lower assistance, especially for older Americans, which will result in people not being able to afford high deductibles and result in fewer people enrolling in health plans. Third, the BCRA would reduce the threshold of the medical care deduction from 10% to 7.5%.

Cuts to healthcare jobs would especially harm the economy. Healthcare has been a major driver of job growth in recent years. The Commonwealth Fund predicts healthcare would lose 30,000 jobs in 2018 under the BCRA. Ultimately, 919,000 healthcare jobs would disappear, which is about 1 of every 22 health jobs.

“While our analysis shows other employment sectors grow initially, by 2026 more than half a million jobs are lost in other sectors of the economy, too,” according to The Commonwealth Fund.

Meanwhile, the Bureau of Labor Statistics released the June jobs report Friday, which said there were 37,000 healthcare jobs added in June, with 26,000 in ambulatory care services and 11,700 at hospitals. So far this year, healthcare job growth has slowed. Healthcare has added 24,000 more jobs on average per month so far in 2017 after adding 32,000 on average per month in 2016.

Also, Memorial Hermann, Summa Health and Hallmark Health all recently announced staffing cuts, which they blamed on declining reimbursements, lower admissions and shrinking operating incomes.

The 37,000 new healthcare jobs in June is positive, but the question is whether that trend remain or will growth slip back down to this year’s average.

The Commonwealth Fund’s report will surely get the attention of economics — and senators. Senate leaders are already trying to figure out ways to tweak the BCRA to get enough conservative and moderate support to pass the legislation. Republicans only have a two-vote majority in the Senate and the current bill doesn’t have enough support for passage.

Uncertainty about what bill — if any — will pass is likely a major factor is slowed healthcare job growth. This latest report about jobs losses if the BCRA becomes law will only deepen the opposition against the bill.

")